You can download the code via this link

https://github.com/mypersonaltrading/VXXVXZ

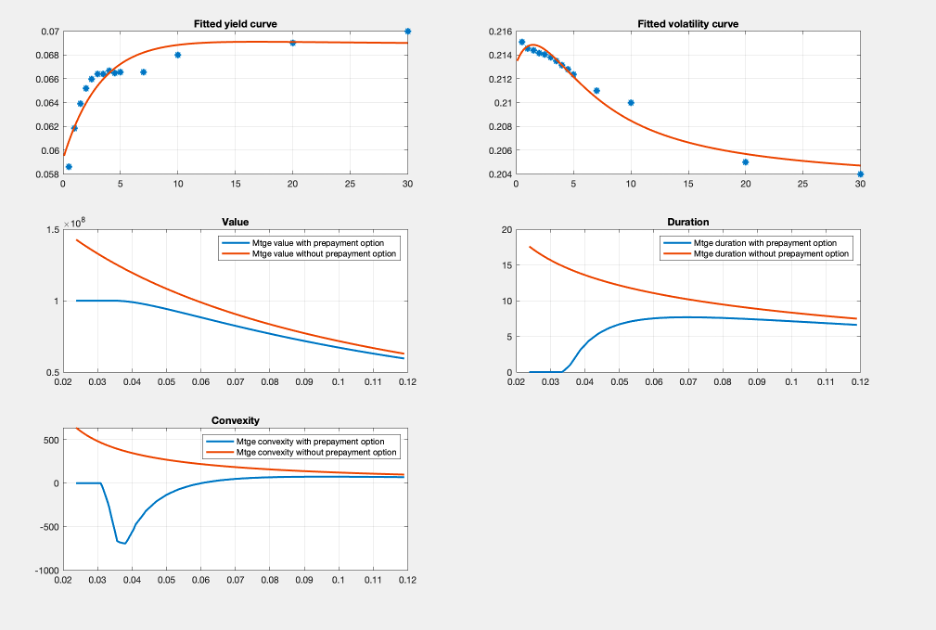

Valuation Methodology

The model used is binomial tree options pricing model, similar to the one used in pricing an American option. First, we use Nelson Siegel model to extrapolate monthly short rate and volatility of a 30-year mortgage. Next, we calculate the cash flow assuming no prepayment by amortizing the principal and interest payments. Then we start from the end of the tree, if the present value of remaining payments at each node is greater than the payoff from outstanding balance, then the option has no value, likewise, if the option is “in the money”, adjust the mortgage cash flow at that node to reflect the prepayment. Finally, we adjust all the cashflow with the matching rate in the short tree then we perform the sensitivity analysis which I will go into details below.

Value

In optimal refinancing, the borrower refinances when interest rates are sufficiently lower than their current rate. This reduces future interest payments, altering the expected cash flows of the mortgage. The present value of these adjusted cash flows is typically lower than that of a mortgage without refinancing, reflecting the reduced interest income for the lender.

Duration

Duration measures the sensitivity of the mortgage’s value to changes in interest rates. It is a weighted average time until all cash flows are received. The plot shows that the mortgage with the prepayment option has a lower duration at lower interest rates. This is because as rates decrease, prepayment becomes more likely, shortening the expected cash flow timeline. The mortgage without a prepayment option has a more stable duration, as it is unaffected by interest rate changes in terms of prepayment risk.

Convexity

Convexity measures the rate of change of duration with respect to interest rates. It indicates how much the duration changes as the yield changes, showing the bond’s price sensitivity to interest rate changes. For the mortgage without the prepayment option, convexity is positive and relatively stable across different interest rates. The mortgage with the prepayment option exhibits negative convexity at lower interest rate levels. This is indicative of prepayment risk; as rates fall, borrowers are more likely to refinance, and the mortgage value does not increase as much as it would for a non-prepayable mortgage. The sharp dip into negative convexity suggests a significant risk of prepayment as rates fall, with the value of the mortgage not rising as fast as it would if prepayment were not an option. This is a key concern for mortgage-backed securities and their investors.

Banks

Banks might include a risk premium in the mortgage rate to compensate for the refinancing risk. This premium would depend on the likelihood of refinancing, which in turn is influenced by the volatility of interest rates and the spread between the current rate and the market rate. If many borrowers refinance, the bank’s expected income from interest decreases. The timing of cash flows becomes unpredictable, complicating asset-liability management for the bank. Banks may also structure mortgages with features like prepayment penalties or variable rate mortgages to mitigate refinancing risk.

Leave a comment