Hello, finished all the midterms and i would like to provide you with a brief update on the current situations.

As the recent geopolitical tension rises and volatility spikes, traders are rolling in to buy downside put protections, triggering a series of market hedging actives by options sellers and a negative put gamma environment. SPX, SPY and various other index options’ term structure rise into backwardation.

Considering the MAG7 stock driving up the entire S&P500 meanwhile the S&P 493 remains flat YTD, and the fact that the P/E of SPX was trading at the very top range for the past 52 weeks from August to September, I think it’s a necessary short term correction from the peak of 4600 level.

According to SpotGamma’s model(could be found on Bloomberg Terminal App), the put gamma is highly concentrated at the 4000 level for SPX options with the highest amount of open interest. Besides, i think it’s worthy to mention the JHEQX fund long 4055 put strike expiring on Dec 29th. The idea behind all of these are that as the market continues to sell off with the uncertainty ahead for the economics and the further rate hikes possibility still on the table.

Looking at the Dec 15 expiration, the put delta notional on SPX options is sitting at about -$423 billion while the call delta notional is less than half of that at around $207 billion. If selling persists, volatility picks up, options sellers have to continue to sell more futures to hedge their books as vanna and charm effect kicks in these 4000 level opened options going into their expiration date around December, exacerbating the equities’ volatility and selling.

If you look at the realized volatility for major indices, it’s been a consistent uptrend since mid September. VIX is trending from 12 to low 20s passing the 16 level that implies daily move of ±1%. However, the gap between realized volatility and implied volatility on the indices continue to widen, which provides us a great opportunity to profit off these premium. The CBOE 1 month implied correlation(COR1M) also started picking up from the beginning of October. These provide some great opportunities for some of the trades i would consider with such rich implied volatility being priced in the indices.

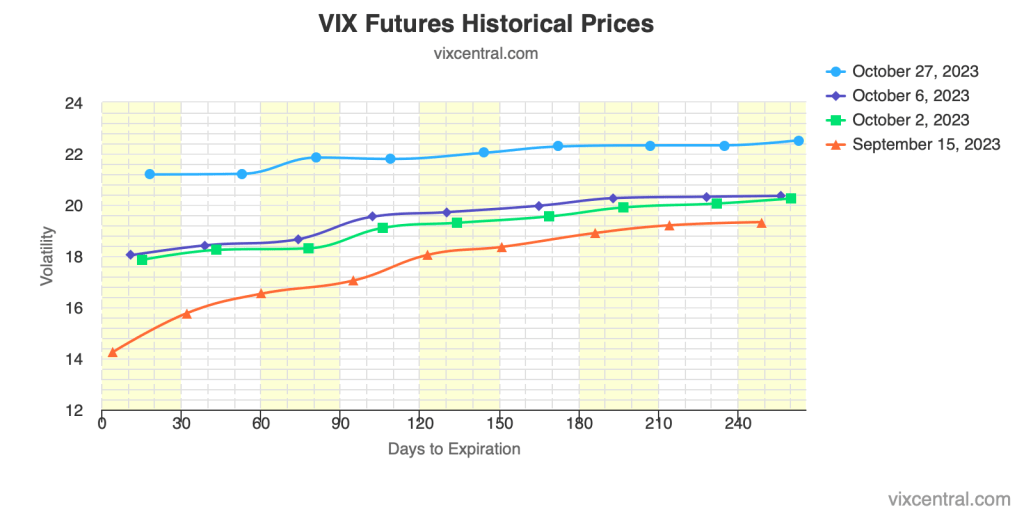

Another conviction that I hold is the flattening of the VIX term structure as shown in graph. On Oct 3rd, the term structure rise to backwardation for the first time since March. But soon after that, it fell back down to a slight contango shape, which is the great opportunity to exit a short volatility trade.

With all of the above in mind.

- I will long skew by buying 4000 put strikes, selling 3500 put for some credit collections, meanwhile selling 4500 calls at a different ratio than the put spread.

- I will short 1 month VIX and long 3 month VIX. (as discussed in this post, the timing matters a lot)

- Calendar spread on SPXW ATM put options(since the put vol is significantly higher than call vol indicated by the 3D volatility surface) shorting nearest Friday expiration and longing the 2 weeks out Friday expiration at the same strike.

On top of these three trades, i will perform analysis on the implied volatility of MAG7 and SPXW ATM options to determine if there’s opportunities for dispersion trade. More on this will be updated soon.

Leave a reply to My opinions on S&P500 going into year end, and my equity index trade idea. – My 100k Simulated Trading Portfolio Cancel reply