These ideas were initially formulated throughout the second week of November, I will keep updating the posts at the bottom to give you a follow up.

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3760365

read this paper first if you don’t really understand what i’m saying

EVERYTHING I WROTE BELOW IS FOR ENTERTAINMENT PURPOSE ONLY, I AM NOT A FINANCIAL ADVISOR. EASTER EGG AT THE BOTTOM OF THE PAGE.

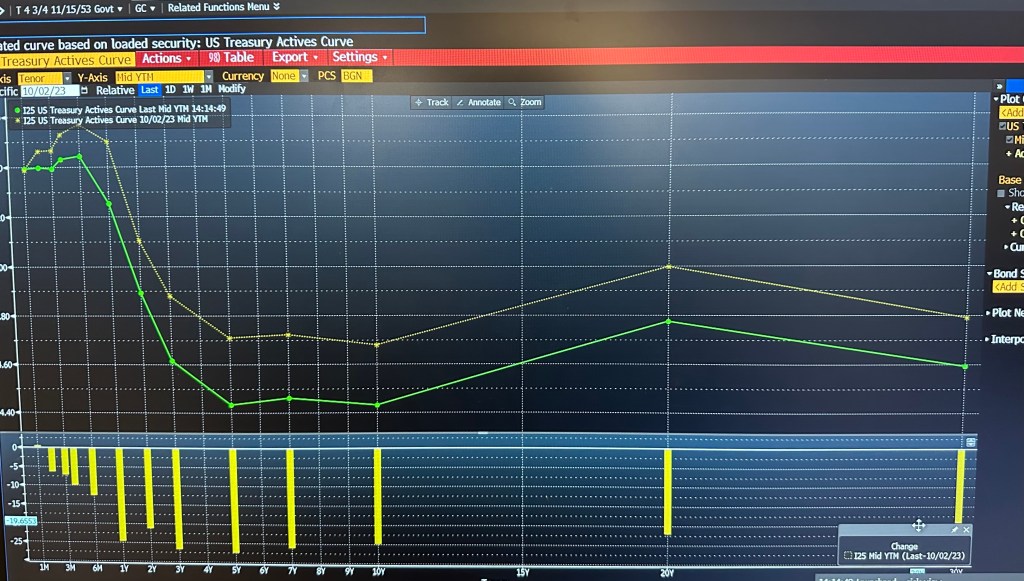

To start off, this post is somewhat a continuation of the previous post where i talked about the equity sell off in October. The funny thing is S&P500 started to rally almost 10% since the beginning of November to the date of writing, which is a greater magnitude than the previous selloff. In a backward looking view, it’s very clear that through various macroeconomic data release(attached at the bottom of this page), they all convey the message that although the economic activities are slowing down across the board especially reflected in the cooler labor market, inflation is tamed well, and the FED is signalling rate pause. In fact, the interest rate swap market has priced in the end of rate hike cycles and rate cutes as early as June 2024…. The yield curve has also shifted lower across all tenors. These all point to one of the directions: we’re finally done with rate hikes and let’s head off to either a minor recession or a high and long rate environment or the combination of both.

On the other hand, i think this rally, is also partially supported by some other factors: volatility selling as a feedback loop; and the massive amount of short put gamma concentrated around 4000&4100 levels on SPX losing their value due to the vanna effect form the quickly evaporating volatility, pushing market dealers to buy back their futures hedges.

—————————

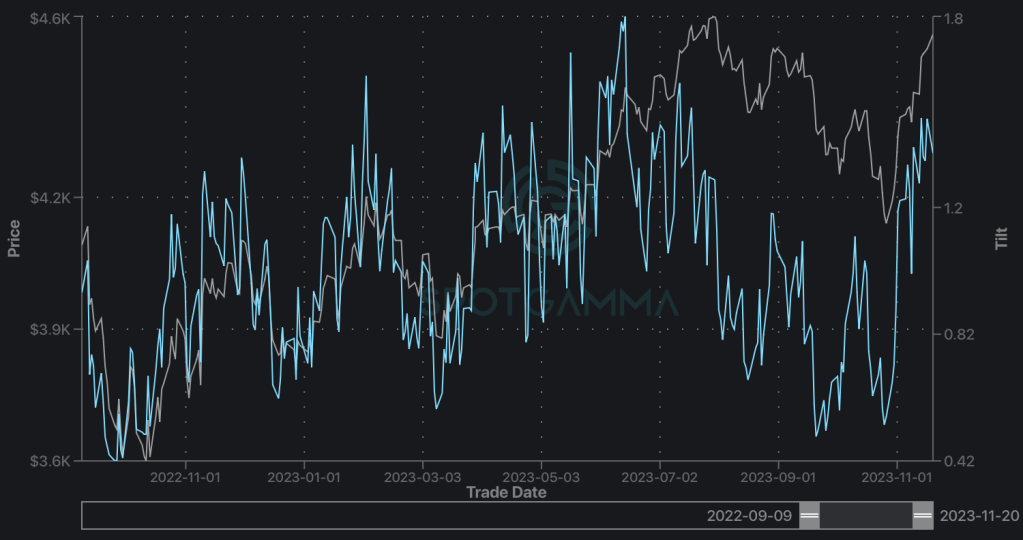

Today( Nov.22), looking at the Dec 15 expiration, the call delta is sitting at 658 billion, put delta is at -160 billion which are sharp contrast compared back in October 30th, call delta=207billion; put delta=-423 billion. These major sentiment shift in the option chain is too pronounced for us to ignore. Speaking of this sentiment shift, it’s also very easily observable at the massive crash of 3M implied volatility starting in the beginning of November, in contrast to the trend up movement of the 60 days realized volatility.(See graph) What’s more the syncing trend down for the three indices VVIX, SDEX, TDEX is suggesting less fear, less hedging demand and lower expectations for future volatility… While we don’t know how many of those newly opened calls are being bought or sold, we can make an educational guess that traders are buying calls to speculate on short term rally, and in the mean time, they’re also selling calls to collect that “dividend”. The reason i think they’re being opened as covered calls is that, again, looking at the option chain, the market has been trading north of 4600 for about a week now, and you can’t really see too many interests on strikes that are higher than 4550 either.

The call gamma has been increasing as market continues to push up, to such amount that it started to subdue volatility in the most recent week, the reasoning behind this is that, as traders and investors sell calls, market makers are buying calls and thus their delta hedging activities will keep the market from fluctuating,(market makers short futures as index go up, and buy it back as index moves down) as the index approach these large strikes concentration, the increasing gamma make this effect more pronounced. This in essence continues to feed the effect into the volatility feedback loop that i mentioned above.

As the last Friday’s November OPEX has passed, based on that idea, I bought a minute amount of short term VIX contracts betting on those call gamma’s disappearance and thus increased volatility. Unfortunately so far, this trade hasn’t gone well( YES, I DO HAVE TIME WHEN I MAKE WRONG JUDGEMENTS lol), i am looking to exit those positions at the end of the week. On the flip side, these open VIX contracts’ value hasn’t lost too much value, besides, these VIX contracts can also act as a short term hedges for the call butterfly and sold call spread positions that i’m trying to slowly build up in the coming weeks, and the longer term volatility strategy that i’ll write in another post.

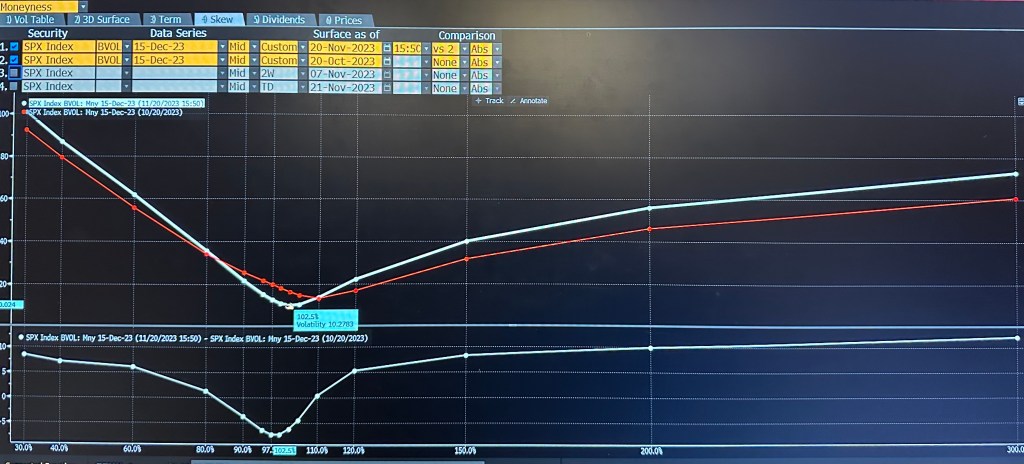

Now let’s talk about my convictions for the call butterfly and short call spread trade. As you can see below, the skew from 90% to 110% moneyness although shifted parallel down in tandem, there’s a minor detail which i personally can’t ignore: the call skew above 100% and especially for those >110% is being bid up(steeper interpolated slope) significantly. This phenomenon is rather strange to me since people aren’t really interested in anything above 4600, not to mention 4600 is the major resistance level this year back in the beginning of August before a massive equity sell off. The call to put ratio graph(with the blue line) as well as the 25D risk reversal also surges which align with the current market sentiment. I think it’s a good idea to start selling calls and continue to roll the positions further along the date, or just do any neutral strategies around 4600 as we’re coming into this strength(does not equal to short). If you’re concerned about shorting vega, i believe looking at the December triple witching call options concentration can help you relax a bit( not to mention the MANY reasons i laid out above), unless there’s a major shifts in those delta and gamma positions, which brings me to the next point: if the index trickle down slightly and implied volatility start to rebound , eventually short sellers have to cover pushing vol back up which is just the basic mean-reversion characteristic of volatility, that’s also the reason i am slowly building up into those positions instead of going all in at once.

If you want to talk about very short term within a week, as realized volatility at 4.7% in this thanksgiving week, and the IV being priced around 9.23% for Dec 1 expiration for ATM strikes, i think there’s still a lot of premium here to sell as long as realized vol continues to grind down, and as long as index doesn’t make a drastic move down. Again, i just want to underline that i think it’s a great opportunity to take advantage of those relatively “bid up” vol.

—————————–

There’re analysts on BI suggesting that recession risk has already been priced in with the current level and P/E of 21.8, although i am always somewhat skeptical about their opinions since i don’t think economy is something you can ever accurately predict, but it makes sense if you compared the P/E at the end of 2022 of 19.5 when earnings suffered, while in 2023, the economy has been surprisingly more resilient than what everybody thinks one year ago( yes, Bloomberg model suggested 100% RECESSION RISK which never happened this year!!!) corporate profits have also been consistently beating analysts’ estimates this year throughout each quarters. Now i am saying this, do i think there’s going to be more upsides in the broader context? The answer is I don’t know. However, I do have some opinions on big tech especially the MAG7 and the small cap such as Russel 2000.

With the massive divergence between the rest of the S&P 500 and MAG7 so far this year, I think tech has shown too much strength, the RSI for SPX and NASDAQ are both in the overbought zone, while Russel 2000 is still far from it. I am long bias on small cap(IWM), and short on MAG7 and QQQ. The weightings for these long short equity ETFs could be inverse market capitalization weighting method, I’d like to use this simply because of how volatile the MAG7 or tech (QQQ) stocks has been and its higher beta compared to small caps(IWM). To express this view, other than just long short equity, you can also do long IWM, while continuously selling calls on QQQ(or MAG7), the reason to do this instead of just simply shorting MAG7 or QQQ is i think it leaves you more room for error in case things go wrong. The amount of delta you’re shorting should be more or less the same as the one that you obtain from the inverse market cap weighting on the underlying.

There’re two major reasons why I want to take this trade.

Small cap( IWM) has been sold in the end of October to a level where we haven’t seen for three year as the result of high interest rates. In a high interest rate environment, these small caps’ WACC go up significantly due to 1.higher risk premium from the increased risk free rate 2. Higher debt to equity ratio in those small cap stocks’ capital structure and thus more pronounced effect on the increment of cost of debt. 3. Higher cost of equity because of the increased risk for the above mentioned reason. While their WACC increases, and being continued to be sold off, I think they’re relatively cheaper being discounted more heavily at the moment. With high possibly of rate pause and rate cut coming soon next year, i am looking forward for the rebound from the intense selling momentum on small cap. In terms of the short side, QQQ not only serve as a hedge, but it also expresses my view on the overvalued tech with the recent AI frenzy. However, as i stress again, the weight is not simply one to one.

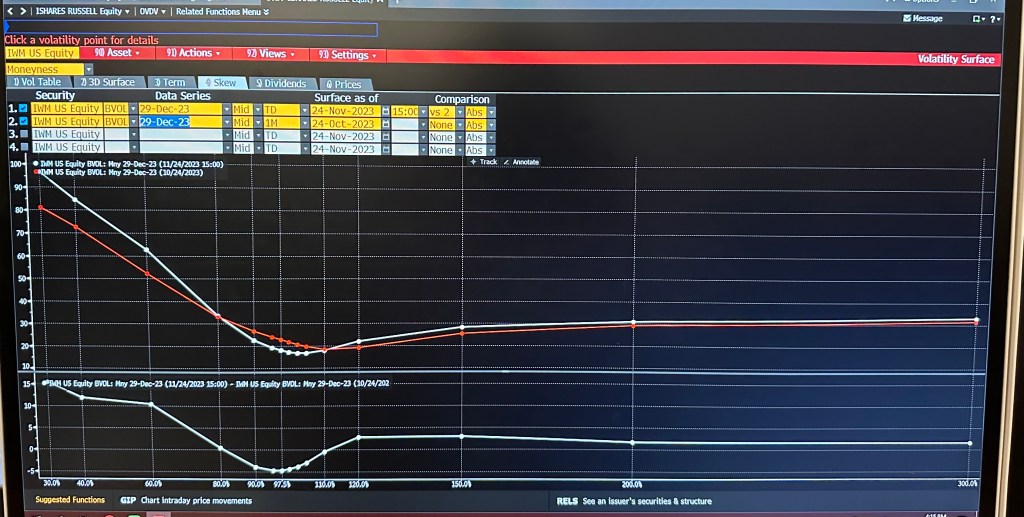

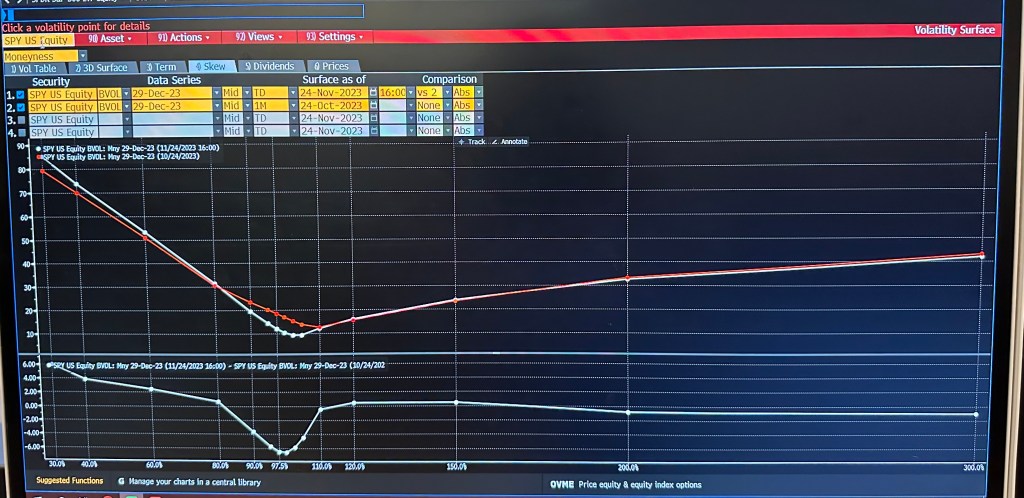

Secondly, this is more of a short term observations, compared the 1 month change in the three skews of IWM, SPY, QQQ on Dec 29, 2023. What do you see? Clearly, IWM’s upside IV is somehow being bid up more than the other two. Does this suggest more upside on IWM? Not necessarily! But when you various factors in mind, it probably makes sense!

In summary:

- Rolling short call spread on a continuous basis.

- Call butterfly around 4600 around mid December, with long VIX hedges

- Short IWM, long QQQ(MAG7). (there’s more than one way to express this view than just buying or selling stocks)

- (THE INTEGRAL BELOW IS NOT 1 if you’re not integrating from minus to plus infinity!!! How can you be so sure about recession? This is a joke of course, since the analysts who model it definitely understand what they’re doing, however, it’s a great example on why you should never fully trust media when it comes to investing and trading!!!)

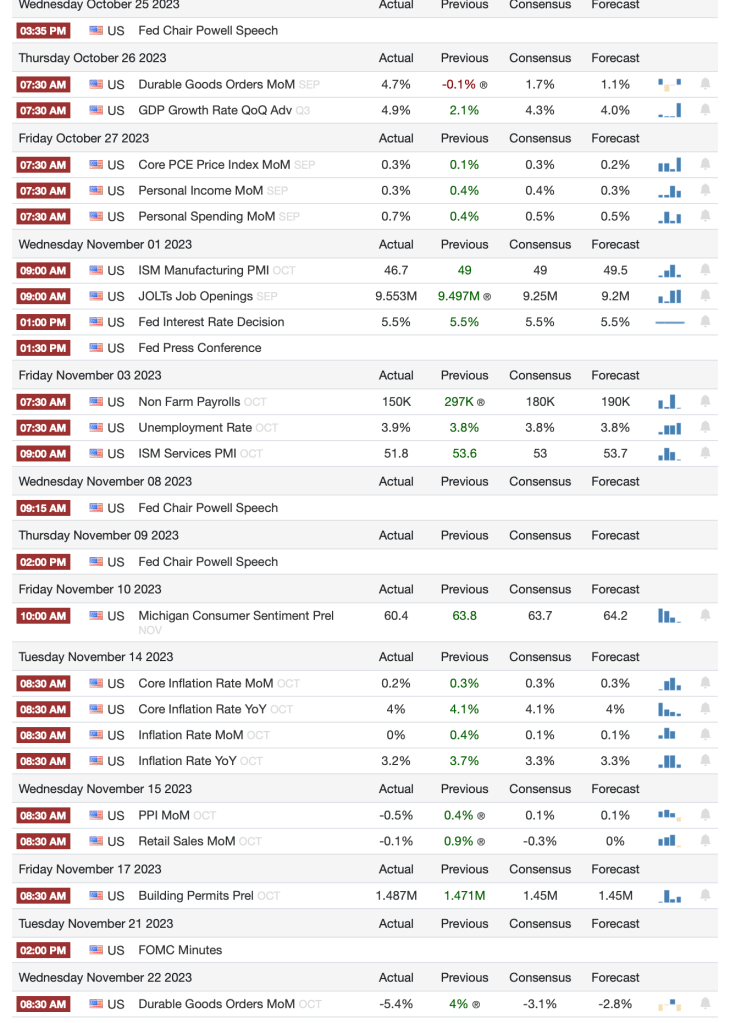

I attached the macro here for your convenience.

Dec 1 note:

A QUICK RECAP:

going into December 1st, the S&P500 closes only 5 points below 4600. This is the timing i’ve been waiting for since the first week of November, I’ve built up 2/3 of my desired positions on the butterfly calls, large size of call spread selling.

My previous call spread for this week unfortunately became a drag for my performance this week, however, the loss is partially negated by my ES hedges and VIX short positions.

The 25 deep in the money IWM 160 calls i entered in the beginning of second week of November has been the major growth contributor to my portfolio this month, generating outstanding return. I do have 3 QQQ short term puts as hedges, I’m averaging down on those put positions to 8 today in the afternoon. The reason i chose 160 strike for IWM is not only just to benefit from the delta, but most importantly: if my view is wrong, and IWM flipped to the downside, my losses would be partially subdued by the increased implied volatility in those contracts.( i’m glad it didn’t happen)

For commodity exposure in my portfolio, I played a bit of oil 2 weeks ago( it was pure gambling on trend following), and it went south from the OPEC cut announcement. i’ve decided i am not touching oil again unless there’s major fundamental shocks in the market. My bullishness in copper and gold is offsetting part of the loss from oil.

FORWARD LOOKING: I’m still bullish on IWM for the reasons below.

- The continued and increased divergence of the 1M change in skew at 1,2 and 3 month maturity among QQQ,SPY,IWM. Today, i obervered massive crash for SPY upside skew as we closes at 4595 on the index. I will sell more upside calls on S&P as a hedge for both QQQ puts’ time decay and downside protection in general.

- Latest positive market reaction from FED’s chair speech and the continuous downward shifting movement in the yield curve.

Lastly, it’s worth noting that the because of January effect for small cap, This year’s December could become a major headwind as investors tend to sell losers as a tax cost reduction strategies, especially with the MAG 7 rallying and having played a huge role as winner this year.

Leave a comment