- EXCEL

I use Black Scholes pricing mode as it’s used in European options style which is what SPXW options pricing is based on. The excel file I use could be found at the bottom of the page. Assuming you’re already familiar with Black Scholes options pricing model, I will briefly explain the process.

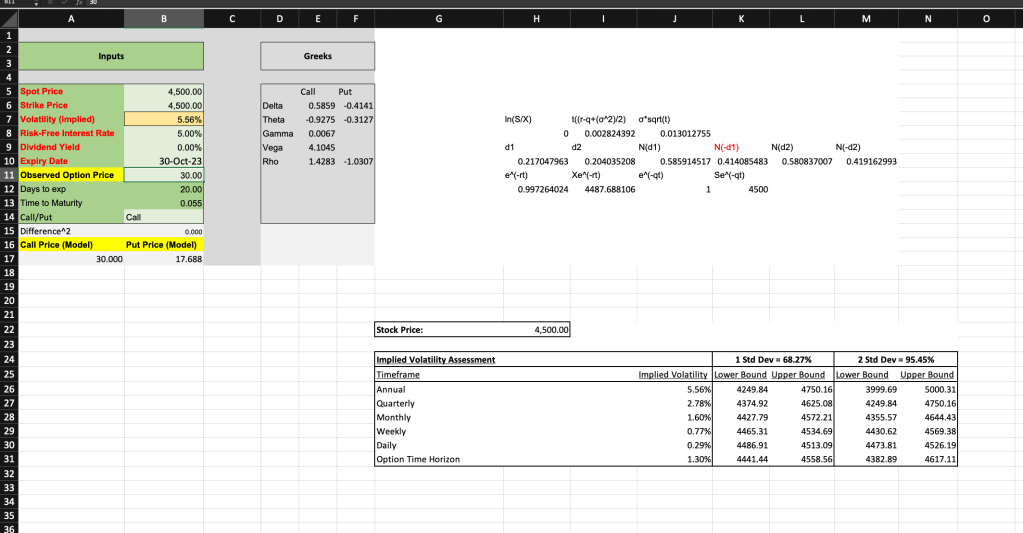

The detailed calculations in the formula could be found in the upper right corner of the excel sheets. User inputs are spot price, strike price, risk-free interest rate which can be approximated by using short term treasury yield, dividend yield which could be found on various resources such as nasdaq and yahoo finance, expiration date of the options, and lastly the observed market option price and options type. NOTE: The formula i use in this file is based on calendar days=365, you can modify it to trading days manually by manually calculating Days to Exp and Time to Maturity.

The second step is to use excel solver to minimize the least square between modelled option price and market options price to value of zero by adjusting the value of Implied Volatility in cell B7. Et Voila, you have the approximated implied volatility. For convenience i also included a table in the lower right corner you can use for reference of the market implied upper/lower bound within 1 and 2 standard deviations.

2. Matlab

Leave a comment